Divorce & Hidden Money: Helga Glock Claims Gaston Glock Started Concealing His Assets

This is the fourth post in the “Divorce & Hidden Money” series.

Mr. Gaston Glock’s creation of the ubiquitous Glock pistol turned him into a billionaire and he is thought to be one of the twenty wealthiest individuals in all of Austria. Mr. Glock’s ex-wife Ms. Helga Glock meanwhile, suspected he is concealing marital assets which could be connected to the couple’s 2011 Austrian divorce.

Ms. Glock therefore used civil law tools in an attempt to detect any marital assets / alleged hidden monies Mr. Glock supposedly possessed. The civil law tools Ms. Glock employed included: 1) her Swiss petition to freeze a UBS bank account reportedly maintained by Mr. Glock in Switzerland; and 2) the March 18, 2013 request for judicial assistance filed at In re application of: H.M.G., U.S. District Court for the Northern District of Georgia, Index No. 13-cv-02598.

MS. GLOCK’S MARCH 18th REQUEST FOR JUDICIAL ASSISTANCE

Ms. Glock’s March 7, 2013 affidavit filed at her request for judicial assistance, claimed Mr. Glock had earlier started hiding and moving personal and corporate assets in anticipation of the couple’s divorce. The March 7th affidavit discussed Ms. Glock’s belief that Mr. Glock was trying to transfer assets out of her reach; and that there had allegedly been a steady flow of assets out of Austria.

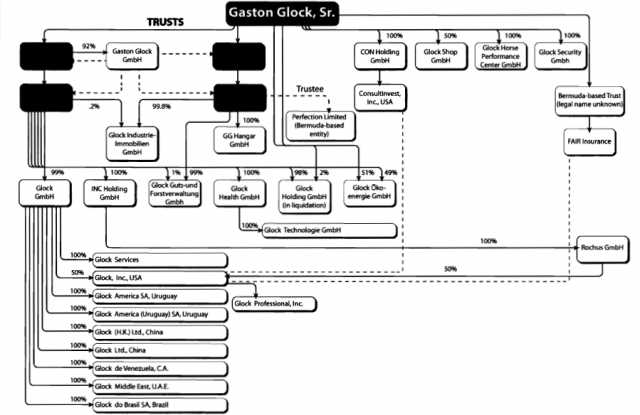

According to the affidavit, there were financial transfers to the above-mentioned UBS Swiss bank account and to bank accounts in Liechtenstein or Luxembourg. Also according to the affidavit, Mr. Glock had a Bermuda trust formed so that it could receive $51 million from “Glock”. The affidavit additionally referred to the “worldwide Glock Group structure” and indicated the structure was thought to be partially depicted by this chart:

A memorandum of law filed with Ms. Glock’s March 18th request for judicial assistance, alleged that Mr. Glock, (i.e. Glock Sr.), was suspected of transferring marital assets through the Glock Group:

“Glock Sr. has erected a complex and opaque structure of holding companies and trusts for Glock affiliated-entities through the world (the ‘Glock Group’) through which he can move and has moved what Ms. Glock contends are marital assets.”

The memorandum additionally alleged U.S.-based entities in the Glock Group were a relevant source of Mr. Glock’s income. According to p.13 of the memorandum, one of these entities Glock, Inc., was thought to be half owned by Rochus GmbH, which supposedly “has no obvious operating role or business-related purpose…”

Page 13 also claimed that:

“The Glock Group is replete with trusts and shell or holding companies, which collectively permit Glock Sr. to manipulate various inter-company transactions and to obscure ownership and accountability.”

Ms. Glock’s March 18th request for judicial assistance sought a court order permitting her to gather the documentary evidence outlined at her demand for document production. Finding Ms. Glock was entitled to discovery, the Court issued its June 3, 2013 Order enabling Ms. Glock to collect evidence from the three entities, Glock, Inc., Glock Professional, Inc. and Consultinvest Inc.

On November 18, 2013, Ms. Glock, Glock, Inc., Glock Professional, Inc. and Consultinvest Inc. filed their Consent Protective Order which the Court granted. The Consent Protective Order governs the production of confidential business documents to Ms. Glock. At its November 18, 2013 Order, the Court also directed that Glock, Inc., Glock Professional, Inc. and Consultinvest Inc. complete their production of documentary evidence to Ms. Glock, no later than January 17, 2014.

On the whole, Ms. Glock’s March 18th request for judicial assistance seems to essentially allege that Mr. Glock could have secretly transferred marital assets by way of:

- trusts;

- shell companies;

- multiple jurisdictions;

- the existing business, Glock Inc.;

- and offshore bank accounts maintained in countries such as Switzerland, Liechtenstein or Luxembourg.

TIPS FOR RECOVERING ASSETS SECRETLY TRANSFERRED OFFSHORE

When a divorcing spouse has actually used the foregoing elements to secretly transfer assets offshore, there can be a border trace and/or other evidence of a money trail. To try to uncover these assets, one may need to use discovery devices along with financial investigators, as suggested at my article “A Primer For Gathering Financial Intelligence”.

An attorney with expertise in tracking assets is usually needed to work with the financial investigators to insure that the investigators supply admissible evidence and/or genuine tips. Ultimately this attorney will also likely have to demonstrate to the Court that the divorcing spouse at issue beneficially owns the secreted assets.

January 1, 2014 Posted in Divorce & Child Support, Divorce & Hidden Money, Financial Institutions, Hidden Money, Swiss Banks, Uncategorized Tagged asset recovery, Gaston Glock, Glock Inc., Glock pistol, Helga Glock, offshore banking, Trusts Comments Off on Divorce & Hidden Money: Helga Glock Claims Gaston Glock Started Concealing His Assets